Bridging Loans for Property in Austria: Tips & Costs for Expats

Bridging finance for property purchase in Austria: When your new home arrives before your old one sells. You've found your dream apartment – but your current property isn't sold yet. This situation is common for many property buyers in Austria – and it has a name: bridging finance. This article explains how it works, what it costs, when it makes sense, and when it should be avoided for expats looking to buy property in Austria.

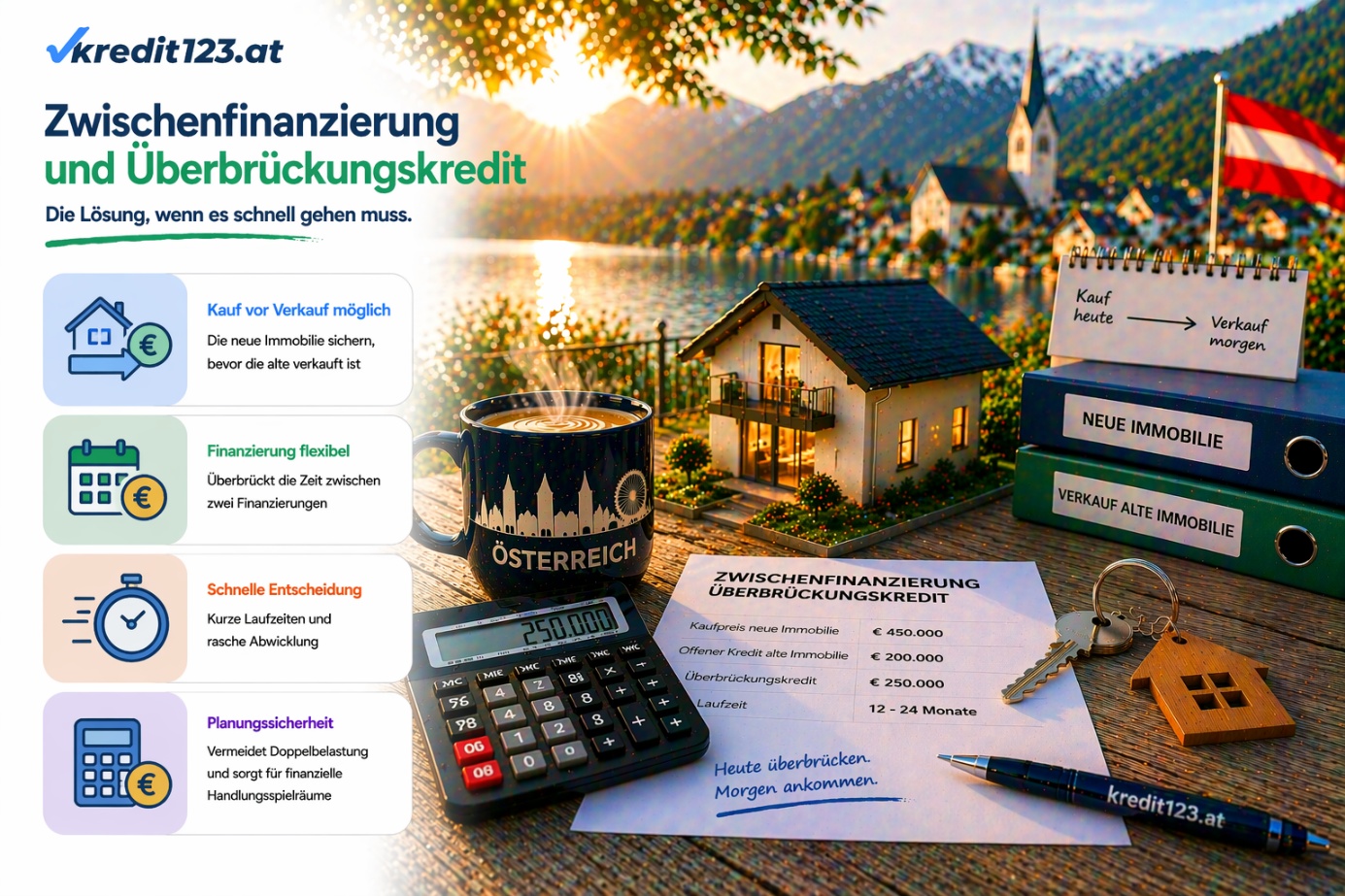

Bridging Loans for Property Purchase in Austria: When Your New Home Arrives Before Your Old One Sells

You've found your dream apartment – but your current property isn't sold yet. Or the loan for your new house is already approved – but the remaining purchase price from the sale of your old apartment is still pending. In this context, we recommend using our mortgage Austria comparison beforehand. This situation is common for many property buyers in Austria – and it has a name: bridging finance (or an interim loan). This article explains how it works, what it costs, when it makes sense, and when it should be avoided for expats looking to buy property Austria.

What is a Bridging Loan – and When Do You Need One?

A bridging loan – also known as an interim loan or bridging finance – is a short-term loan that bridges a time gap between two cash flows.

In real estate, this gap typically occurs in three situations:

Situation 1: Purchase Before Sale – You want to buy property Austria and have planned to use equity from the sale of your current property. However, your current property hasn't sold yet. The buyer for your new home won't wait until your old one is sold. Result: You need the purchase price payment now – but the money will only become available later.

Situation 2: Tranche Payments for Developer Purchases – When buying a new-build apartment from a developer, purchase price installments are due as construction progresses. You have your equity tied up in your current apartment – which you plan to sell only after the new build is completed. In the meantime, the developer installments must be covered by a bridging loan.

Situation 3: Inheritance or Gift is Forthcoming – But Not Immediately – An inheritance or gift has been announced – but not yet paid out. The purchase can and should happen now. The expected funds will arrive in a few months.

In all three situations, the basic principle is the same: the necessary capital is available – but not yet accessible. Bridging finance closes this time gap. Before committing, you should compare property loans to find the best conditions for your property loan Austria.

How a Bridging Loan is Structured

The Classic Structure

A bridging loan is typically a short-term, bullet loan – meaning:

The term is short: typically six to twenty-four months

During the term, only interest is paid – no principal repayment

At the end of the term, the entire loan amount is repaid in one go – from the proceeds of the sold property or the receipt of expected funds

This structure has a crucial advantage: the monthly burden is low during the bridging phase because only interest is paid on the outstanding amount.

Illustrative Example:

New apartment: 380,000 Euros purchase price

Equity from own savings: 80,000 Euros

Expected proceeds from sale of old apartment: 200,000 Euros (not yet available)

Required long-term loan: 100,000 Euros

Structure:

Long-term bank loan: 100,000 Euros (25-year term, normal annuity)

Bridging loan: 200,000 Euros (12-month term, interest-only)

Equity: 80,000 Euros

Monthly Burden During the Bridging Finance Phase:

Annuity from long-term loan: approx. 500 Euros

Interest on bridging loan (at 4.5%): approx. 750 Euros

Total burden: approx. 1,250 Euros per month

After selling the old apartment: Bridging loan is fully repaid. Remaining burden: only the annuity of the long-term loan of approx. 500 Euros. Illustrative calculation without guarantee.

The Combined Structure: Bridging and Long-Term Finance from One Source

Many banks offer a combined solution – bridging finance and a long-term loan are approved simultaneously and processed in a coordinated manner.

This has the advantage that the entire financing requirement comes from a single source and the processing is coordinated. Disadvantage: You are tied to one institution – a comparison of several offers is still advisable. If you already have existing loans, you should also consider refinancing.

What a Bridging Loan Costs

Bridging loans are more expensive than standard mortgage Austria options. This is due to structural reasons – short term, higher risk for the bank, administrative effort.

Interest Rate Comparison in Austria

Typical interest rates for bridging loans in Austria 2026:

Financing Type | Effective Interest Rate approx. |

|---|---|

Normal Variable Mortgage | 3.0 – 3.8 % |

Normal Fixed 10-Year Mortgage | 3.5 – 4.3 % |

Secured Bridging Loan | 4.0 – 5.5 % |

Unsecured Bridging Loan | 5.0 – 7.0 % |

Indicative values without guarantee. Actual conditions depend on creditworthiness, collateral, and institution.

The higher interest rate for bridging finance is for the short term. For a bridging loan of 200,000 Euros over twelve months at 4.5% interest:

Monthly interest payment: approx. 750 Euros

Total interest costs over 12 months: approx. 9,000 Euros

This is the price for the flexibility to buy property Austria now without having to sell the old one first.

Additional Financing Costs

In addition to the interest rate, other fees may apply depending on the structure:

Cost Type | Timing | Typical Amount |

|---|---|---|

Processing Fee | Upon closing | 0.5 – 1.5 % of loan amount |

Land Register Entry (Pfandrecht) | For secured financing | 1.2 % of loan amount |

Valuation Fee | For property valuation | 500 – 1,500 € |

Notary Fees | For Land Register (Grundbuch) processing | 500 – 2,000 € |

For an unsecured bridging loan, the land register-related costs are omitted – but the interest rate is higher. Use our ancillary costs calculator to keep track of all fees for your real estate financing Austria.

What Collateral Banks Require

A bridging loan represents an increased risk for the bank – because repayment depends on a future event that has not yet occurred. The bank therefore secures itself.

Collateral 1: Lien (Pfandrecht) on the New Property – The most common model – the new property is encumbered with a lien that secures the bridging loan. However, this is only possible if the new property is already owned by the buyer or at least a registered purchase offer (verbüchertes Kaufanbot) exists.

Collateral 2: Assignment of the Purchase Price Claim – If an old property has already been sold but the purchase price has not yet been paid out, the bank may require the assignment of the purchase price claim. This means: The buyer of the old apartment pays the purchase price directly into a trust account of the bank – not into the seller's account.

Collateral 3: Lien (Pfandrecht) on the Old Property – If the old property has not yet been sold and has no outstanding loan, the bank can register a lien on the old property in the Land Register (Grundbuch). This secures the bridging loan through the existing property assets.

Collateral 4: Combination of Several Collaterals – In practice, banks often combine several collaterals – for example, a lien on the new property plus assignment of the purchase price claim from the old one.

The Most Important Risks of Bridging Finance

A bridging loan only works if the assumptions on which it is based materialize. If not, a real problem arises.

Risk 1: The old property does not sell for the expected price

This is the most common risk. If you plan your bridging loan based on an expected sale proceeds of 300,000 Euros, and the property then only sells for 260,000 Euros, there is a gap of 40,000 Euros – which must come from somewhere.

How to mitigate this risk: Conservatively estimate the expected sale proceeds – plan for 10 to 15 percent below your desired price rather than at the peak. And build a buffer into the financing structure for your expat mortgage.

Risk 2: The old property does not sell in time

The bridging loan has a term – typically twelve to twenty-four months. If the old property is not sold within this period, the bridging loan must be extended – which means additional costs – or other means of repayment must be found.

How to mitigate this risk: Realistically assess the marketing duration. In Vienna and Graz, well-located apartments often sell in a few months. In rural areas, it can take longer. Choose the term of the bridging loan accordingly.

Risk 3: Double burden is not sustainable

During the bridging finance phase, you pay both interest on the bridging loan and possibly operating costs or rent for the old apartment – plus the annuity of the long-term loan for the new property. This double burden must be serviceable monthly from your income.

How to mitigate this risk: Calculate the maximum monthly total burden during the bridging phase – and check whether your household income can bear it.

Risk 4: The inheritance or gift is delayed or falls through

If the bridging loan is based on an expected inheritance or gift, this is the most uncertain foundation. Inheritances can be contested, and gift promises can change.

How to mitigate this risk: Only plan on legally secured funds – not on verbal promises. If possible, legally formalize the gift in advance.

When a Bridging Loan Makes Sense – and When It Doesn't

Makes sense if:

The property to be sold is in a sought-after location and can realistically be sold within six to twelve months.

The expected sale proceeds are significantly higher than the bridging loan amount – providing sufficient buffer for price negotiations.

The monthly double burden during the bridging phase is clearly sustainable.

There is a concrete intention to purchase the new property – not just a theoretical consideration.

The conditions of the new property are so good that waiting for the sale of the old one would be economically disadvantageous.

Does not make sense if:

The property to be sold is in a weak demand area and a sale is uncertain.

The expected sale proceeds are barely above the bridging loan amount – no buffer available.

The monthly double burden pushes household income to its limit.

The new property would still be available later – there is no time pressure.

The buyer for the old apartment has not yet been found, and there are no concrete interested parties.

Also ask yourself: Rent or Buy? Sometimes a strategic interim step to renting is the safer choice.

Alternatives to Classic Bridging Finance

Before taking out a bridging loan, it's worth exploring alternatives – which can sometimes be cheaper or simpler.

Alternative 1: Negotiate a Longer Transition Period in the Purchase Agreement – If the seller of the new property is flexible, a later handover date can be agreed upon in the purchase contract. This completely eliminates the need for bridging finance.

Alternative 2: Overdraft Facility on Existing Property – If the old property is debt-free or partially debt-free, an overdraft facility can be set up on the existing lien (Pfandrecht). This is more flexible than a classic bridging loan.

Alternative 3: Equity from Other Sources – Sometimes bridging finance can be avoided by activating other equity sources – liquidating securities accounts, surrendering life insurance, family support.

Alternative 4: Sell First – Then Search – The simplest alternative: First sell the old property, then search for the new one. This completely eliminates the timing problem – but requires temporary accommodation.

The Process of a Bridging Loan in Practice

Purchase Decision and Initial Consultation: The new property has been found, the purchase offer is in place. Now is the right time for the first discussion.

Define Financing Structure: Together with the advisor, the structure is determined: how much long-term loan, how much bridging finance, what term for your property loan Austria.

Bank Approval: The bank reviews both financing components simultaneously. Approval heavily depends on proof of marketability of the old property.

Purchase of the New Property: After approval, the new property is purchased. Interest payments on the bridging loan run parallel to the new annuity.

Sale of the Old Property: The old property is marketed. The sale proceeds flow directly to repay the bridging loan.

Repayment: Upon receipt of the sale proceeds, the bridging loan is repaid and the lien (Pfandrecht) is released.

What Banks Specifically Check for Bridging Loans

Marketability of the Old Property

This is the most critical review point. The bank wants to ensure that the old property can actually be sold within the planned term at the assumed price. Valuation reports or existing purchase interests are helpful.

Sustainability of the Double Burden

The bank checks whether the household can monthly bear the interest payments on the bridging loan plus the annuity of the long-term loan – from current income, especially important for an expat mortgage.

Equity Buffer

A sufficient equity buffer gives the bank security that no financing gap will arise even with a lower sale proceeds.

Required Documents for Bridging Finance

Document | Purpose |

|---|---|

Purchase Agreement/Offer for New Property | Proof of purchase |

Land Register (Grundbuch) Extract for New Property | Collateral valuation |

Land Register (Grundbuch) Extract for Old Property | Current encumbrances |

Valuation Report for Old Property | Realistic market value |

Proof of Income | Sustainability of double burden |

KSV Extract (Credit Report) | Creditworthiness |

How kredit123.at Helps with Bridging Finance

Bridging finance is one of the more complex financing tasks – because two transactions must be coordinated simultaneously. We structure the overall financing and ensure that both parts are aligned. We know the institutions that routinely offer bridging loans for real estate financing Austria.

At the same time, we always first check whether bridging finance is truly necessary – or if there is a cheaper alternative. Sometimes a simple adjustment of the purchase contract date is the more elegant solution.

Non-binding initial consultation for bridging finance and interim loans – we examine your specific situation → kredit123.at

Frequently Asked Questions about Bridging Finance (FAQ)

How long can a bridging loan run?

Typically six to twenty-four months. Some institutions go up to three years – but the longer the term, the higher the total interest costs for your expat mortgage.

Does the old property have to be debt-free?

Not necessarily – but an existing loan reduces the available net value. The net proceeds after repayment of the existing loan are the relevant figure.

What happens if I cannot repay on time?

The bank can extend the term – for additional costs. In extreme cases, it can realize the collateral.

Can I also use bridging finance for an inheritance?

Generally yes – if the inheritance is legally secured and the timing of the payout is clearly foreseeable.

Are interest payments tax deductible?

For rented investment properties, interest can be tax-relevant. For owner-occupied properties, deductibility is limited.

Checklist: Before Taking Out a Bridging Loan

Sale proceeds of the old property conservatively estimated – buffer of 10–15% planned

Marketing duration of the old property realistically assessed

Term of the bridging loan chosen accordingly – with a buffer

Monthly double burden calculated: new annuity + bridging loan interest

Double burden is sustainable from current income

Alternatives checked: Is a later handover date possible?

Collateral structure clarified: lien on new property, old property, assignment

Valuation report for old property available

Targeted institutional comparison planned for your mortgage Austria

Notary appointments for both transactions coordinated

Conclusion: Bridging Finance is a Tool – Not a Last Resort

Bridging finance is not a sign of financial weakness – it is a legitimate tool for individuals transferring their property assets. Properly structured, it enables the purchase of the right property at the right time.

The key lies in a realistic assessment of the marketing duration and the sale price. Those who approach this in a structured way – with an advisor who coordinates both transactions – turn a complex timing problem into a manageable financing task.

Are you planning to buy property Austria while your old one is not yet sold? Let our experts support you in finding the optimal bridging finance solution. Request a non-binding consultation now and gain financial security for your expat mortgage.

This article is for general information purposes only and

Useful Tools for Your Financing

Related Articles

Mortgage Calculator Austria: How Much Can You Borrow Based on Your Salary?

Mortgage Calculator: How much mortgage can I get with my salary in Austria? "How much mortgage can I get with my salary?" — this is the first question almost everyone asks before even starting to look for a property. The answer depends on more than just your salary. This article explains the exact calculation, provides concrete tables for various income situations, and shows what you can do to increase your maximum loan amount when looking for a property loan Austria.

Read more

Immobilienkredit Österreich 2026: Leitfaden zur Finanzierung

Immobilienkredit in Österreich 2026: Der ultimative Schritt-für-Schritt LeitfadenDieser Leitfaden ist die wohl fast vollständige Antwort auf alle Frag...

Read more

Eigenleistung beim Hausbau in Österreich: Muskelhypothek nutzen

Eigenleistung beim Hausbau in Österreich: Was Banken als Eigenkapital anerkennen – und wie man den Immobilienkredit damit optimiertWer selbst baut und...

Read moreQuestions about your financing?

Our experts advise you personally and find the optimal solution for your property financing in Austria.