Investment Properties in Austria | Property Loan in Austria 2026

Financing investment properties in Austria: What private investors need to know. Buying a rented apartment, collecting rental income, and having the loan repaid – it sounds simple. This guide helps expats navigate the complexities of getting a mortgage in Austria and buying property.

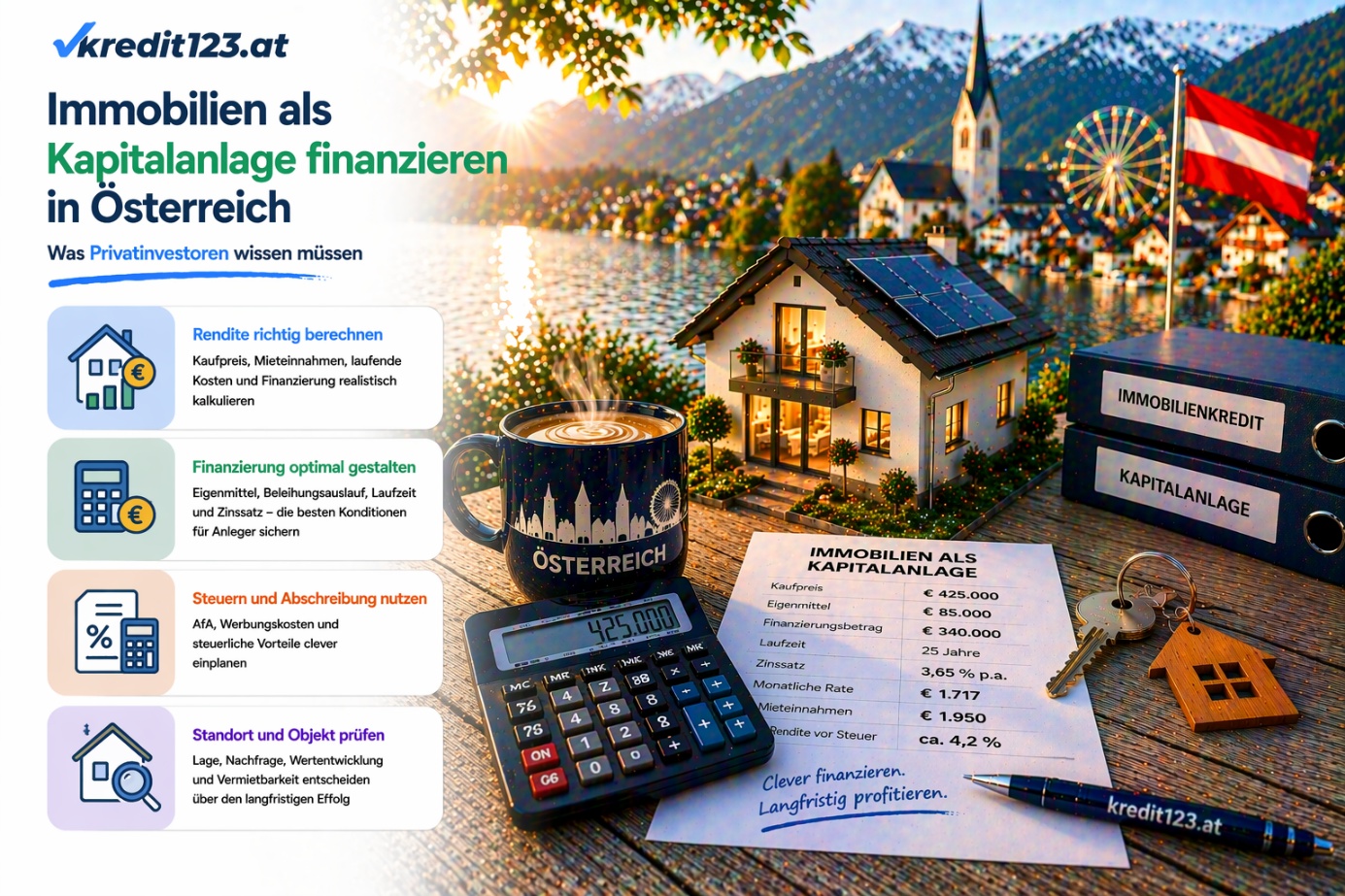

Financing Investment Properties in Austria: What Private Investors Need to Know

Buying a rented apartment, collecting rental income, and having the loan repaid – it sounds simple. And the basic principle is indeed not complicated. But between the basic principle and a truly functional investment property, there are many details that determine success or failure. This article explains how private investors in Austria can properly finance an investment property, how banks assess these differently than owner-occupied purchases – and what mistakes almost everyone makes in their first investment.

The following article is not an investment recommendation!

Why Investment Properties are Becoming More Attractive Again in 2026

After two challenging years – interest rate hikes in 2022/23, purchase price corrections in 2023/24 – the environment for real estate investors has noticeably improved in 2026. If you start a loan comparison now, you will find that the conditions for a property loan Austria are significantly more attractive than recently.

Three developments are converging:

Lower Interest Rates: The ECB has initiated the interest rate reduction cycle. Financing costs are significantly below the 2023 peak – variable loans are back to three to four percent effective. This significantly improves the cash flow of investment properties.

Corrected Purchase Prices: In many Austrian locations, purchase prices fell by ten to twenty percent in 2023 and 2024. Those who buy now are buying cheaper than at the peak – and may benefit from a recovery.

Rising Rents: While purchase prices have fallen, rents in most Austrian cities have continued to rise – due to indexation, high demand, and limited supply. This significantly improves the rental yield mathematically.

The combination of more affordable purchase prices, lower financing costs, and increased rental income makes 2026 a more interesting time to enter the investment property market than in previous years. Before you commit, however, you should accurately calculate the acquisition costs with our ancillary costs calculator.

The Basic Principle: How External Financing Works for Investment Properties

The special feature of investment properties is the leverage effect of external financing – also known as leverage. It is the most powerful tool for a real estate investor and at the same time the most dangerous if not understood.

The Leverage Effect in Comparison

A simple illustrative example clarifies the power of external capital in real estate financing Austria:

Feature | Scenario A (100% Equity) | Scenario B (25% Equity) |

|---|---|---|

Purchase Price | 200,000 Euro | 200,000 Euro |

Equity | 200,000 Euro | 50,000 Euro |

Loan Amount | 0 Euro | 150,000 Euro |

Interest Rate / Term | - | 3.5 % / 25 Years |

Net Rental Income p.a. | 8,000 Euro | 8,000 Euro |

Loan Installment p.a. | 0 Euro | approx. 9,000 Euro |

Return on Equity | 4.0 % | approx. 15 % (incl. Repayment/Appreciation) |

Simplified illustrative example without guarantee. No taxes, no maintenance, no vacancy periods considered.

What the leverage effect shows: With the same equity of 200,000 Euro, the investor in the second scenario can buy four properties with 50,000 Euro equity each – instead of one property without a loan. The total return on invested capital is significantly higher – but the risk increases proportionally. The leverage effect works in both directions: if property values fall, the leveraged investor loses a higher percentage than the unleveraged one.

How Banks Assess Investment Properties Differently from Owner-Occupied Properties

This is the first major difference that many first-time buyers don't know: banks treat investment properties more strictly than owner-occupied properties – in several respects. If you already own a property, you should also regularly consider a loan refinancing to optimize interest costs.

Higher Equity Requirements

For owner-occupied properties, there are no longer statutory minimum equity ratios prescribed since the expiration of the KIM-V (Kreditinstitute-Immobilienfinanzierungsmaßnahmen-Verordnung - Regulation on Real Estate Financing Measures for Credit Institutions). Banks can decide individually. For investment properties, most Austrian institutions still require at least 25 to 30 percent equity – often more. The reason: with an owner-occupied apartment, the borrower has a strong personal interest in paying the installment – they live in it. With an investment property, this personal interest is absent. The risk of default is statistically higher.

Rental Income Not Fully Credited

Those who rent out an apartment have rental income – that's clear. But banks do not credit this income 100 percent as income. Typical deductions are 20 to 30 percent – for vacancy, maintenance, and rent default risk. This means: for a monthly rent of 1,000 Euro, the bank calculates approximately 700 to 800 Euro of creditable income. This is less than the investor expects – and has direct implications for the affordability calculation.

Investor's Creditworthiness Also Counts

For an owner-occupied apartment, the property is the collateral and the borrower's income is the source of repayment. For an investment property, a third element is added: the tenant. If the tenant does not pay or the apartment is vacant, the investor must cover the loan installment from their own income. Therefore, in addition to the property collateral, the bank also checks: Does the investor have their own income that can cover the installment in an emergency – even without rental income?

Interest Rate May Be Higher

Some institutions grant loans for investment properties at slightly higher interest rates than for owner-occupied properties – due to the higher risk profile. This is not universal, but observable in practice. A targeted comparison is therefore even more important for investment properties than for owner-occupied purchases when looking for a mortgage Austria.

The Yield Calculation: What Really Matters

Yield is not just yield. There are several key figures that investors need to know – and which provide very different insights. Whether the purchase is worthwhile can often only be guessed after a comparison with the Rent or Buy? calculator.

Gross Rental Yield

The simplest key figure: Gross Rental Yield = (Annual Net Rent ÷ Purchase Price) × 100. Example: Apartment for 250,000 Euro, net rent 900 Euro/month results in a gross rental yield of 4.32 %. It serves for quick comparison but ignores all costs.

Net Rental Yield

More realistic – but still without financing: Net Rental Yield = ((Annual Net Rent − Running Costs) ÷ Total Investment) × 100. Here, property management (3-5%), maintenance (1-2%), and vacancy reserves (5-8%) are deducted. In the example above, the yield often drops to approx. 3.02 %.

Cash Flow Yield (with Financing)

The most important key figure for externally financed investment properties: Monthly Cash Flow = Rental Income − Loan Installment − Running Costs. A negative cash flow means that the investor has to make monthly additional payments. This can still be sensible with high appreciation but requires liquidity.

Return on Equity

The most comprehensive key figure: Return on Equity = (Total Annual Return ÷ Equity Invested) × 100. It shows how efficiently your capital works, considering the leverage effect.

For all yield calculations: Tax implications are individual and significant – they belong in the calculation but can only be correctly captured with a tax advisor.

What Makes a Good Investment Property – The Most Important Criteria

Location: The Most Unchangeable Feature

For an investment property, the location is even more important than for an owner-occupied property – because it's not the investor who has to live with it daily, but a tenant needs to be found, and the appreciation potential is crucial.

Location | Character | Gross Rental Yield approx. | Risk |

|---|---|---|---|

Vienna Inner Districts | High purchase prices, stable demand | 2.5–3.5 % | Low |

Vienna Outer Districts | Moderate prices, good demand | 3.5–4.5 % | Low–Medium |

Graz | Growing university city, good demand | 4.0–5.0 % | Medium |

Linz | Industrial city, solid demand | 4.0–5.5 % | Medium |

Salzburg | High prices, tourist overlap | 3.0–4.0 % | Medium |

Rural Areas | Favorable prices, weak demand | 5.0–7.0 % | High |

Guideline values without guarantee. Actual yields depend on the specific property.

Property Size and Condition

In practice, smaller apartments (30–60 m²) in Austria often show better rental yields than larger ones. Regarding condition: New builds offer low maintenance and better energy efficiency with a lower initial yield. Existing properties attract with higher yields but carry renovation risks and are often subject to the strict Mietrechtsgesetz (MRG – Tenancy Law Act).

Tenancy Law: An Austrian Specific

In Austria, there is comparatively strong tenant protection law – the Mietrechtsgesetz (MRG). It regulates what rents may be charged, under what conditions a tenant can be terminated, and who is responsible for which repairs.

Full MRG Application: Applies to old buildings (built before 1953) where the main rent is limited. Rent increases are severely restricted here.

Partial MRG Application: Applies to many existing apartments – tenant protection yes, but rent can be agreed more freely.

No MRG Application: Applies to new builds after 2001, single-family homes, holiday apartments. Here, rent and termination are largely freely negotiable.

The Financing Structure for Investment Properties – What Works Well

For successful real estate financing Austria, the structure is crucial. An equity ratio of 30% ensures better conditions and a positive cash flow. For the term, "longer" is often better to reduce the monthly burden and optimally utilize the leverage effect. Whether fixed-rate or variable depends on the strategy; mixed models (e.g., 10 years fixed) often offer the best balance of security and flexibility for your expat mortgage.

Tax Fundamentals for Investment Properties

Rental income is subject to income tax. However, loan interest, the Absetzung für Abnutzung (AfA) (depreciation) of 1.5% p.a., and operating costs are deductible. Upon sale, the Immobilienertragsteuer (ImmoESt) (real estate income tax) of 30% is levied on the profit. Professional tax planning is essential here.

Typical Mistakes When Buying Your First Investment Property

Only looking at the gross rental yield.

Not calculating the cash flow thoroughly.

Not planning for a vacancy buffer.

Ignoring the tenancy law (MRG).

Bringing too little equity.

Neglecting the tax aspects.

Only inquiring with one bank for your mortgage Austria.

Not having an exit strategy.

How kredit123.at Specifically Supports Private Investors

Investment properties are an area where an independent credit broker provides particular added value – because the financing structure is more complex, bank requirements are stricter, and the differences in conditions between institutions are greater. We know the Austrian banks that are keen to finance investment properties and strategically structure your portfolio. This is especially helpful for expats looking to buy property Austria.

Request a non-binding consultation

Frequent Questions from Private Investors

How many investment properties can I finance? This depends on your overall creditworthiness. There is no legal upper limit, but internal bank limits for total exposure.

Can I use rental income as income? Yes, but with deductions of 20-30% for a security buffer.

Is a negative cash flow a problem? Not if your other income covers the difference and the appreciation justifies the strategy.

Checklist: Before Buying Your First Investment Property

Complete yield calculation: Gross, Net, and Cash Flow calculated

Vacancy buffer planned: Two to three months of rent loss reserved annually

Equity at least 25–30% of the total investment

Sufficient personal income: Can the loan installment be covered even without rental income?

Tenancy law for the specific property checked: MRG application, rent limits

Tax advisor involved: Tax yield calculation and structuring discussed

Exit strategy defined: What happens if the investment doesn't work out?

Compared multiple banks: Not just your main bank – targeted institutional comparison for your expat mortgage.

KSV (Kreditschutzverband von 1870 - Austrian Credit Protection Association) checked in advance

Grundbuchauszug (land register extract) of the property checked: No unresolved encumbrances

Conclusion: Investment Properties in Austria 2026 – Interesting, But Not Passive

A well-selected, properly financed investment property in an Austrian city is once again an attractive investment in 2026. The combination of lower interest rates, corrected purchase prices, and rising rents creates better entry conditions than in the last two years. But real estate is not a passive investment. It requires careful selection, financing structure, tax planning, and management. This is key for expats looking to buy property Austria.

Do you want to invest your capital profitably in real estate? We support you in finding the optimal financing for your project and compare the best offers on the market for you. Let us maximize your return together.

This article is for general information purposes only and does not constitute individual financial, tax, or legal advice. Yield figures are illustrations without guarantee. Tax issues for investment properties are complex and individual – they must be clarified with a licensed tax advisor. Credit decisions are always made by the respective institutions at their own discretion.

Useful Tools for Your Financing

Related Articles

Mortgage Calculator Austria: How Much Can You Borrow Based on Your Salary?

Mortgage Calculator: How much mortgage can I get with my salary in Austria? "How much mortgage can I get with my salary?" — this is the first question almost everyone asks before even starting to look for a property. The answer depends on more than just your salary. This article explains the exact calculation, provides concrete tables for various income situations, and shows what you can do to increase your maximum loan amount when looking for a property loan Austria.

Read more

Bridging Loans for Property in Austria: Tips & Costs for Expats

Bridging finance for property purchase in Austria: When your new home arrives before your old one sells. You've found your dream apartment – but your current property isn't sold yet. This situation is common for many property buyers in Austria – and it has a name: bridging finance. This article explains how it works, what it costs, when it makes sense, and when it should be avoided for expats looking to buy property in Austria.

Read more

Immobilienkredit Österreich 2026: Leitfaden zur Finanzierung

Immobilienkredit in Österreich 2026: Der ultimative Schritt-für-Schritt LeitfadenDieser Leitfaden ist die wohl fast vollständige Antwort auf alle Frag...

Read moreQuestions about your financing?

Our experts advise you personally and find the optimal solution for your property financing in Austria.