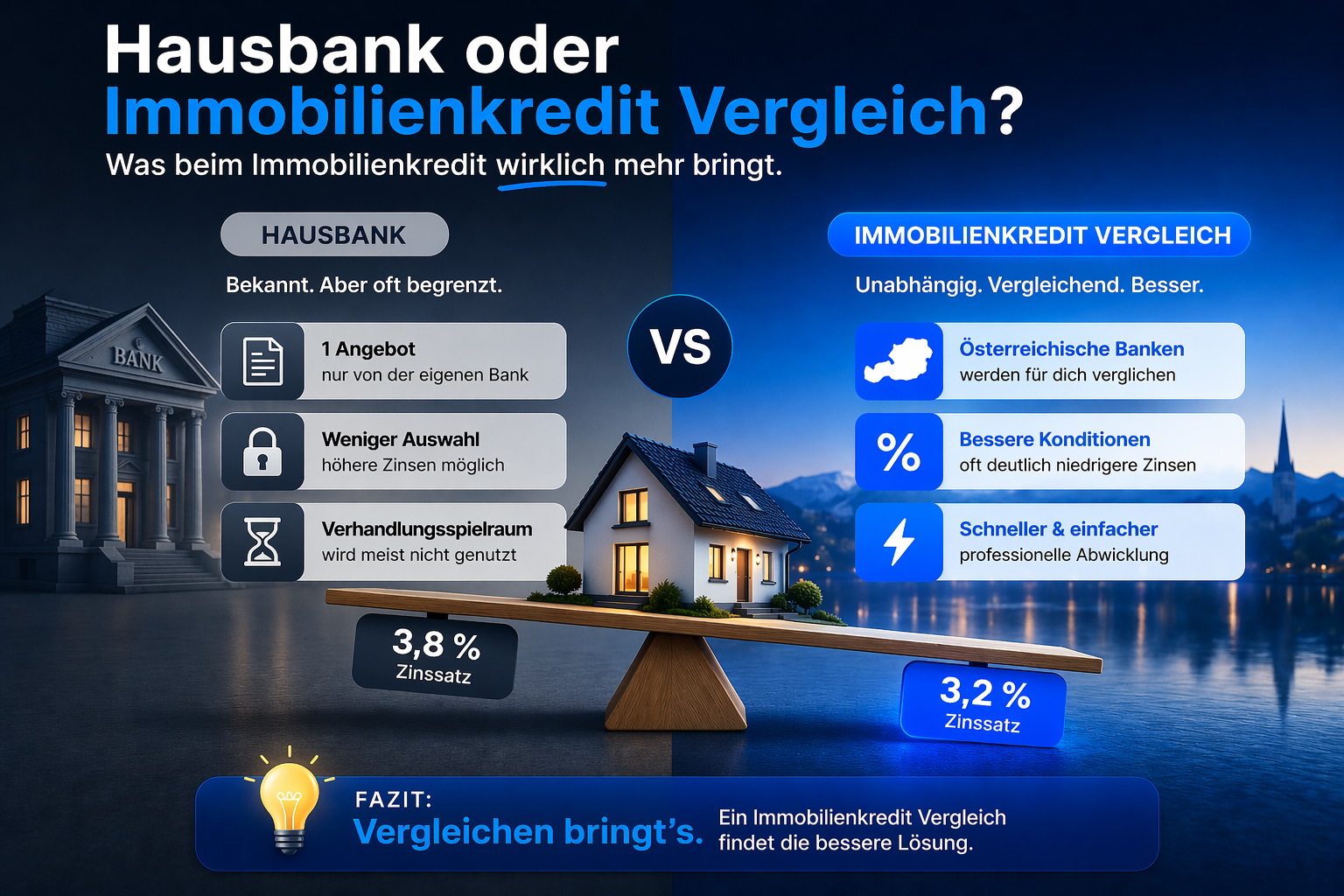

House Bank or Mortgage Broker? A Comparison for Your Mortgage in Austria

House bank or mortgage broker? What truly offers more for your mortgage in Austria. Most people in Austria who take out a mortgage first inquire with their house bank. This is understandable — the relationship is familiar, the process known. But is it always the smartest decision? This article soberly compares both approaches, with figures and without advertising. If you want to know directly how much you can save, use our mortgage comparison calculator.

House Bank or Mortgage Broker? What truly offers more for your mortgage in Austria

Most people in Austria who take out a mortgage Austria first inquire with their house bank. This is understandable — the relationship is familiar, the process known. But is it always the smartest decision? This article soberly compares both approaches, with figures and without advertising. If you want to know directly how much you can save, use our mortgage comparison calculator.

Why the House Bank is the First Choice — and Why It's Not Always Optimal

Your house bank knows you. It knows how much is in your account, how regularly your salary comes in, and whether you've used an overdraft in the past. This builds trust — on both sides.

What many don't know: This familiar relationship is an advantage for the bank, not just for you. A bank that knows no comparison is being made has no economic incentive to offer its best deal. The margin — the bank's markup on the reference interest rate — is the bank's profit. The higher the margin, the better for the bank, the more expensive for you.

This is not an insinuation, but market logic. And it explains why borrowers who only inquire with one bank generally receive worse conditions than those who actively compare. Often, it's also worth looking into loan refinancing if you already have an ongoing financing.

What a House Bank Offers — and What It Doesn't

Strengths of the House Bank

Known Creditworthiness: The bank knows your account history and needs to check less. This can speed up the process.

Existing Relationship: In case of problems — payment deferral, rate adjustment, special repayment — a personal relationship with the advisor is helpful.

Everything from one source: Current account, savings products, loan, and insurance with the same institution — a convenience argument for some customers.

Local Presence: A local branch is important for people who prefer face-to-face advice.

Weaknesses of the House Bank

No Market Comparison: The house bank only offers its own products. You won't find out what other institutions offer at better conditions — unless you ask yourself.

Conflict of Interest: The bank advisor works for the bank, not for you. Their goal is to sell the bank's product — preferably with a good margin.

Standardized Assessment: Those with an unusual profile — self-employed, temporary employment, foreign currency income, foreign nationality — are often assessed according to standard criteria and rejected, even though other institutions might be more flexible. This is particularly relevant for an expat mortgage.

Limited Product Range: Some banks do not have their own building society solutions, no promotional loan cooperations, or no suitable mixed interest rate model.

What an Independent Mortgage Broker Does — and What It Doesn't

A mortgage broker is not a bank advisor. They do not work for a bank, but as an intermediary between the borrower and the credit institution. Their legal basis in Austria is the Hypothekar- und Immobilienkreditgesetz (HIKrG) (Mortgage and Real Estate Credit Act), which obliges credit intermediaries to transparency, duty of advice, and disclosure of remuneration.

What a Good Mortgage Broker Specifically Does

Market Overview: An experienced broker knows the current conditions of many banks and institutions — not just one. They know which institution is particularly open to which profile.

Profile Creation and Preparation: Before inquiring with banks, the borrower's profile is professionally prepared. A complete inquiry increases the probability of approval.

Targeted Institution Selection: Instead of indiscriminately inquiring with five banks — which burdens KSV inquiries (Austria's credit bureau) — the broker specifically inquires with the institutions that are the best fit.

Negotiation: The broker negotiates in the interest of the borrower. They know the margins and where there is room for maneuver.

Support until Disbursement: A good broker accompanies the process until the final loan disbursement — including coordination with the notary.

What a mortgage broker is not: They do not decide on the loan — the bank does. They do not guarantee approval. And they do not replace the notary or lawyer for legal questions regarding the purchase agreement when you buy property Austria.

The Direct Comparison: House Bank vs. Mortgage Broker

Criterion | House Bank | Independent Mortgage Broker |

|---|---|---|

Number of Offers | 1 (own product) | Many institutions |

Interest Position | Not independent | Borrower |

Negotiating Position | Low (no comparison) | Strong! (Competitive offers) |

Profile Preparation | Standardized | Individual |

Costs | No direct fee | Often borne by the institution |

Complex Profiles | Limited | Broker's strength |

What the Difference Means in Numbers

The decisive argument is not abstract — it can be calculated. The margin that a bank adds to the reference interest rate is the negotiable part of the interest rate. An experienced broker can often reduce this margin by 0.2 to 0.5 percentage points, making your mortgage Austria more affordable.

Example Calculations for Interest Savings:

Loan Amount | Term | Interest Difference | Total Savings |

|---|---|---|---|

€200,000 | 25 years | 0.2 % | approx. €6,500 |

€200,000 | 25 years | 0.4 % | approx. €13,000 |

€300,000 | 25 years | 0.3 % | approx. €14,500 |

€350,000 | 25 years | 0.5 % | approx. €28,000 |

Example calculations for illustration without guarantee. Actual savings depend on the individual case.

Even in the most conservative scenario, we are talking about over €6,000 in savings. Use the loan calculator on kredit123.at to calculate what small interest differences mean for your specific case. Don't forget the ancillary purchase costs – our ancillary costs calculator will help you here.

When is the House Bank the Better Choice?

It would be dishonest to claim that a mortgage broker is always the better option. There are situations where the house bank actually comes out on top:

If the house bank already makes a very good offer: Especially for long-standing, wealthy customers. A comparison is still useful to put the offer into perspective.

If the relationship with the bank is strategically important: Those who finance their company through the same bank can have an overall benefit.

If speed is more important than optimization: In very tight buying situations, a quick commitment from the house bank can be an advantage when you buy property Austria.

In all other cases — and that is the vast majority — an independent comparison is the better starting point. This is especially true for an expat mortgage.

What a Mortgage Broker Costs — and Who Pays

Mortgage intermediaries are obliged under the HIKrG to transparently disclose their remuneration. In practice, the commission is often borne by the mediating credit institution — not by the borrower. The bank pays the broker a referral commission because it has gained a customer.

For the borrower, this means: The advice often costs nothing directly — and the savings through better conditions remain with you. Whether costs are incurred is communicated in writing before each consultation at kredit123.at.

What to Look for When Choosing a Mortgage Broker

Trade License and Registration: In Austria, credit intermediaries need to be registered in the Firmenbuch (Commercial Register) and with the FMA (Financial Market Authority).

Independence: An independent broker has access to a wide range of institutions.

Experience: Specifically ask about experience with your situation (e.g., self-employed, an expat mortgage).

Network: A broker with contacts to lawyers and notaries is more valuable for the entire process, especially when dealing with the Grundbuch (land registry) and other legal aspects of buy property Austria.

The Conclusion: Comparison is Not an Option, but a Standard

Nobody buys a car from the first dealer without comparing. The same should apply to a mortgage — often the biggest financial decision in life. The house bank is a possible provider, but an independent mortgage broker ensures that you get the best offer on the market for your mortgage Austria.

Those who compare are informed borrowers. And informed borrowers generally pay less for their home loan.

Inquire without obligation now

Secure the best interest rates for your real estate financing in Austria. Our experts compare the best offers for you and negotiate the best conditions.

This article is for general information only and does not constitute individual financial or credit advice. All example calculations are illustrations without guarantee. Specific conditions and remuneration agreements are communicated individually and in writing.

Useful Tools for Your Financing

Related Articles

Immobilienkredit umschulden Österreich 2026: Zinsen & Tipps

Immobilienkredit umschulden in Österreich 2026: Für wen es sich wirklich auszahltkredit123.at · Ratgeber · Thema: Umschuldung Immobilienkredit Österre...

Read more

Immobilienkredit Rechner: Wie viel Kredit bei welchem Gehalt?

Immobilienkredit Rechner: Wie viel Kredit bekomme ich mit meinem Gehalt in Österreich?"Wie viel Kredit bekomme ich mit meinem Gehalt?" — das ist die e...

Read more

Mortgage Calculator Austria: How Much Can You Borrow Based on Your Salary?

Mortgage Calculator: How much mortgage can I get with my salary in Austria? "How much mortgage can I get with my salary?" — this is the first question almost everyone asks before even starting to look for a property. The answer depends on more than just your salary. This article explains the exact calculation, provides concrete tables for various income situations, and shows what you can do to increase your maximum loan amount when looking for a property loan Austria.

Read moreQuestions about your financing?

Our experts advise you personally and find the optimal solution for your property financing in Austria.